Dec. 30, 2021 5:34 AM ETTidal ETF Trust – SP Funds S&P 500 Sharia Industry Exclusions ETF (SPUS)AMAGX, AMANX, AMAPX, AMIGX, AMINX, AMIPX, HLAL, SPRE, SPSK, SPY5 Comments4 Likes

Summary

- SPUS is developed to comply with Sharia guidelines and has been certified by an authority on Islamic finance.

- This ETF holds about 200 members of the S&P 500, excluding overleveraged stocks and stocks from certain industries.

- Compared to the S&P 500 it is overweight tech, but comparable with other Sharia-ETFs like HLAL. I will compare SPUS to SPY and HLAL in this article.

- For non-Muslims who sympathize with the industry exclusions, this ETF can provide diversification to investors who are underweight tech with large financials or utilities, as those sectors are excluded.

- This ETF may have lower interest rate sensitivity, as it excludes companies that have large exposure to interest-bearing assets and liabilities.

A few years ago, I wrote an article on various ETFs and other funds that were designed to build their portfolios using religious criteria. Religious ETFs, along with ESG ETFs, could be grouped together as ethics based investments for those who want broad market exposure while avoiding stocks of companies engaging in behavior contrary to your ethics. I’ve also written on a sustainable development goals ETF, The iShares Global Impact ETF: How Sustainable Development Can Be Unsustainable, which is an ETF aimed at investors who are looking to use sustainable development philosophies to pick investments. If you are an investor who wishes to take into account some sort of ethical worldview when deciding on investments and are considering some sort of values ETF, then it’s important to understand the implementation of it along with the goals. The aphorism of don’t judge a book by its cover has many analogous equivalents beyond books, with the equivalent here being don’t judge a fund by its name.

While the headline goals of the ETF may broadly align with your worldview, the implementation methodology may not be as strict as you’re hoping for or might even be counterproductive. For example, the iShares Global Impact ETF (NASDAQ:SDG), which has environmental responsibility as one of its goals, excludes nuclear despite it having low CO2 emissions comparable with solar while promoting biofuel which isn’t very green when taking into account the land, water, and energy use that goes into production, transport, as well as emissions from combustion.

Christian ETFs

In my previous religious-based investment article, How to Invest According to Your Religious Values: ETFs and Mutual Funds, I looked at a few Christian focused ETFs: the equity-based Inspire Global Hope ETF (BLES) and Inspire Corporate Bond Impact ETF (IBD), along with the more narrowly focused Global X S&P 500 Catholic Values Index ETF (CATH).

Inspire has expanded its biblically focused offerings to include the Inspire Global 100 ETF (BIBL), Inspire Small/Mid Cap Impact ETF (ISMD), Inspire International ESG ETF (WWJD), Inspire Tactical Balanced ESG ETF (RISN), Inspire Faithward Large Cap Momentum ESG ETF (FEVR), and Inspire Faithward Mid Cap Momentum ESG ETF (GLRY). There is also a new biblically focused ETF provider, Timothy Plan, which offers the Biblically Responsible US Large/Mid Cap Core ETF (TPLC), High Dividend Stock ETF (TPHD), US Small Cap Core ETF (TPSC), International ETF (TPIF), US Large/Mid Cap Core Enhanced ETF (NYSEARCA:TPLE), and High Dividend Stock Enhanced ETF (NYSEARCA:TPHE). If you are a Christian, you may wish to check out those funds.

Islamic Mutual Funds

At the time of my previous religious based investing article, no US listed Islamic-focused ETFs existed; however, I did analyze Amana Growth Fund (AMAGX) focusing on US and international growth stocks and the Amana Income Fund (MUTF:AMANX) consisting of US and international dividend stocks.

I will briefly mention the Amana Income Fund near the end of the article, as I think it’s the most different in terms of holdings compared to the SP Funds S&P 500 Sharia Industry Exclusions ETF (SPUS) and the Wahed FTSE Shariah USA ETF (HLAL) as both those 2 ETFs and the Amana Growth Fund are overweight tech.

SP Funds and Sharia Compliance

SP Funds is an ETF company by Sharia Portfolio, a boutique investment advisory firm, focusing on Sharia-compliant ETFs. They offer: the SP Funds S&P Global REIT Sharia ETF (SPRE), SP Funds S&P 500 Sharia Industry Exclusions ETF, and the SP Funds Dow Jones Global Sukuk ETF (SPSK). Sukuks are a special type of asset-backed financial instrument similar to a bond which pays out a share of profits derived from the asset rather than a determined amount of interest.

Probably the most notable investment-related exclusion that Islamic law mandates is that of interest. Investors who wish to adhere to Islamic law cannot invest in regular bonds as well as certain industries that profit off of interest such as banks. Businesses that make use of credit may also be prohibited to invest in if their leverage is “excessive”. As virtually all businesses use some form of credit, guidelines were developed to inform Muslim investors about how much debt is reasonable for a company that they own shares of to have, as well as setting limits for income earned from prohibited sources (like bank account interest).

Investment exclusion guidelines for SP Funds are made in compliance with Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) standards with Imam Dr. Omar Suleiman serving as the spiritual advisor to SP Funds. The SPUS fund and SPRE funds are both certified as being Sharia-compliant by an Islamic financial advisory and auditing firm.

S&P500 Sharia Industry Exclusions ETF

- Expense Ratio: 0.49%

- Dividend Yield: 0.97%

- Holdings: 210

- Index and/or Selection Universe: S&P500

- Top, and Top 10 Holdings: 12.2% and 47%

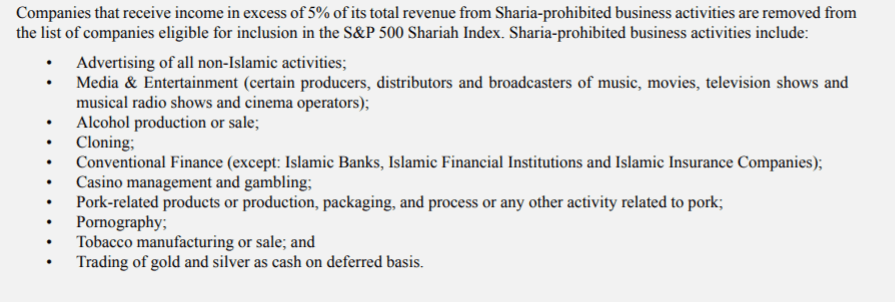

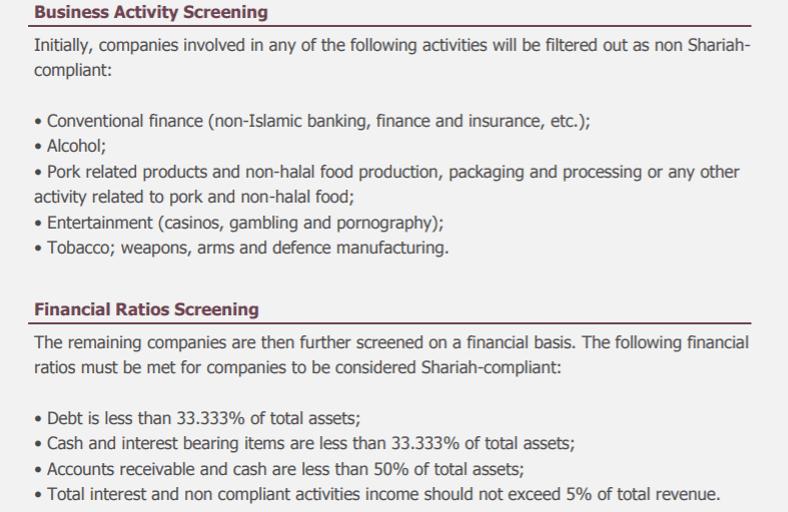

Which industries are excluded?

Source: Prospectus

Alcohol / Tobacco – Alcohol and tobacco are generally considered prohibited by most scholars.

Gambling – Islamic law prohibits gambling and speculation.

Weapons / Defense – Islamic law forbids sales of weapons to enemies and aggressors. Selling to businesses and others who have a legitimate need for defense can be permissible but it’s easier to exclude it entirely than analyzing the customer bases of each weapons maker.

Pornography – Pornography goes against Islamic morality laws, so investing in porn companies is prohibited.

Pork Products – Islamic dietary law prohibits the consumption of pork which is also a prohibition in Jewish dietary law. Investing in producers of pork is prohibited.

Highly Leveraged Businesses and conventional financials (including credit cards).

Islamic banks, Islamic financials and Islamic insurance companies are exempt.

An Islamic-compliant enterprise should not make use of interest-based debt financing. This presented a problem for Muslims who were looking to invest in publicly listed stocks since virtually all businesses in Western countries make use of interest-based financing or make money off of interest. Exemptions and guidelines were developed allowing Muslims to invest in lightly leveraged companies and companies where only a small portion of revenues (<5%) comes from interest income and other prohibited sources. I will go into more detail further below.

The Catholic Church has also frowned upon charging interest and prohibited it prior to the 16th century. It still teaches against excessive interest rates, although its limitations are much less restrictive than in Islam, where making any money off of interest could be viewed as sinful.

Cloning – Cloning is generally prohibited (although some scholars say there may be exemptions for therapeutic cloning).

Music, Cinema, or Broadcasting – The ETF has most of the previous criteria in common with other religious-based investment offerings. I’d heard of the other exclusions but never heard of a reason why music, cinema or broadcasting would be limited under Sharia. So I had to look a bit further into this exclusion.

Why music? Many (maybe even most) Islamic scholars hold that music is forbidden, either in all cases or with some exemptions and other restrictions (such as depending on the instruments used). Even in schools of Islam that allow music, generally any sort of music that has some sort of sexualized or “immoral” theme (which is pretty common in modern music) or expresses a message contrary to Islam will still be prohibited. There is some debate about whether music is prohibited as music isn’t explicitly mentioned in the Quran. Most scholars when arguing on music look to the hadiths (which are collections of reported statements by Islam’s Prophet, Mohammed) – the hadiths are often used as part of Islamic legal rulings, especially when something isn’t explicitly mentioned in the Quran. The authenticity of certain hadiths prohibiting music are disputed and the remaining hadiths only regulate certain types of music; however, most hadiths that mention music are critical of it, making it open to interpretation.

Certain producers, distributors, broadcasters of movies, music, television shows or musical radio shows are also prohibited. Movies are generally not prohibited, except by a minority of clerics (cinemas were banned in Saudi Arabia, Taliban Afghanistan, and other countries like Iran might not ban movies entirely but still have a censorship office). If a movie contains ‘sinful’ elements (which could include music), then it may be prohibited. Many modern Western movies do contain sexualized scenes for example, so most Western movie producers / distributors will be excluded. Even some animations may be prohibited depending on the storyline and other factors.

It’s not just Islam trying to regulate music and movies: certain groups of Christians and Jews do or have tried to regulate, restrict or condemn certain types of music and other forms of media.

Trading of gold/silver/currencies futures and forwards – This is considered speculation, especially as many futures traders don’t intend to take delivery.

Leverage Screens

Source: Prospectus

The ETF screens based on financial metrics limiting the debt, cash + interest bearing items, cash + accounts receivables, and total interest + non-compliant income, are respectively less than 33.333%, 33.333%, 50%, and 5%.

The portfolio will exclude overleveraged companies and companies that have a large amount of quick assets. This would have the side-effect of limiting interest rate sensitivity depending on how the debt and interest bearing cash/investments are structured (i.e. the specific interest rates, fixed vs. floating, credit risk, duration, etc.) as the market value of debt will go down when interest rates rise and increase when interest rates fall.

It will also limit companies that have too much in cash and liquid assets which could instead be used to invest in productive assets or returned to shareholders (in the form of dividends or share repurchases). There is a prohibition against trading shares of companies that have 100% liquid assets, unless done at par value rather than the market value. The allowable amount of liquid assets as a percentage of total assets is debatable and somewhat arbitrary, but the figures used by SPUS are reasonable when compared with other Sharia investing guidelines.

The reason 1/3 (33.333%) is used as a limit (for being excessively leveraged or holding excessive cash + short term investments) is because of a narration in the Hadiths (sayings of Prophet Mohammed) about what percentage is excessive in relation to inheritance law.

Sa’d said: “I was stricken by an ailment that led me to the verge of death. The Prophet came to pay me a visit. I said, ‘O Allah’s Apostle! I have much property and no heir except my single daughter. Shall I give two-thirds of my property in charity?’ He said, ‘No.’ I said, ‘Half of it?’ He said, ‘No.’ I said, ‘One-third of it?’ He said, ‘You may do so, though one-third is also excessive.”

Bukhari, Book 8, Volume 8, Hadith 725 (Laws of Inheritance)

While that figure isn’t explicitly related to the percentage of debt or quick assets that are excessive, and the investment limitations set are somewhat arbitrary, you’ll often see ratios in Sharia-compliant investment standards that are based around thirds (sometimes rounded down to 30% to make sure there’s some safety so you don’t approach excessive). Ideally no interest-based assets or liabilities should be used, but doing so would be challenging in the modern financial system. Most Western companies will see no reason to limit their financing options and even large companies with majority Muslim boards in majority Muslim countries will find it challenging to have no debt, no interest paying assets and earn no income from any prohibited source.

Income Purification

Most Western companies don’t consider Sharia compliance when deciding what sorts of business activities to engage in. Almost every publicly traded business in US exchanges will likely have some non-Sharia compliant income (i.e. income from prohibited business activities or interest).

Does this mean that Muslims are prohibited from owning any stock that has an interest bearing account and investments in the form of treasury notes? A Muslim would be prohibited from owning interest paying notes directly, but would it be ok if it’s done through a corporation they own?

Recognizing that requiring business to have zero “impure” income will exclude practically every publicly listed company, Islamic scholars have decided that while the goal should be getting as close to zero impure income as possible, that anything under 5% could be allowed. The 5% figure is somewhat arbitrary, but seems to be what most Sharia investment guidelines use (although one standard uses 10% and Malaysia’s standards have multiple levels of prohibited income that may be permissible up to 5-25% depending on the circumstances).

It is not only necessary to limit impure income to revenues according to whatever standard is used, in this case 5%, but it is also required to purify the impure income if you receive dividends. Generally capital gains are not required to be purified whereas dividends are paid out directly from the accumulated impure income and do require purification. I’m not sure what the case would be for a company that decides not to pay dividends and instead spends that cash on share buybacks indirectly providing capital gains to investors. It might be possible that it could serve as a loophole to avoid purification of dividend income, although there’s probably a Sharia opinion elaborating on this and the interpretation of this issue might be subject to disagreement among scholars.

SP Funds provides a table containing the purification factor of each ETF, based on how much of dividends are considered illicit. The purification factor can be multiplied by the value of dividends received and that amount should be donated to charity to cancel out the impure income.

The values given are estimates as there can be different ways to calculate it. If you are looking to purify your income, you may want to consult a trusted religious authority. If you’d want to take extra precaution, you might want to round up or add some sort of contingency factor in case the estimate is lower than the amount of purification necessary if determined via manual review, which you can discuss with your religious advisor.

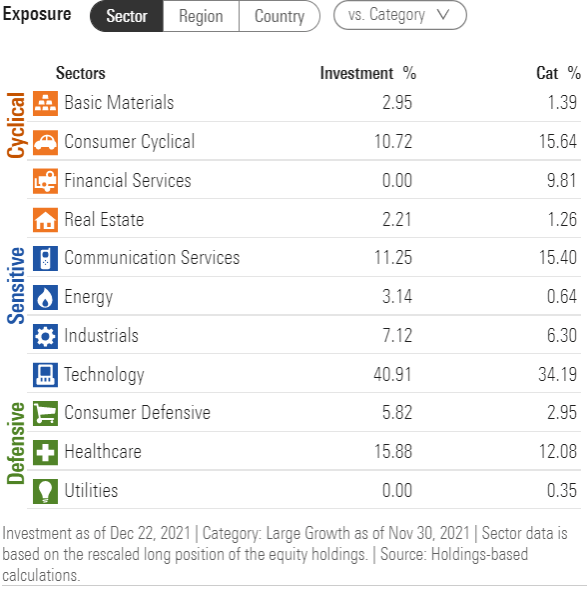

How does it compare with the S&P 500?

SPUS

Source: Morningstar

SPY

Sector weights:

- No financials, utilities in SPUS vs. 13% and 2.5% in SPY

- Overweight technology: 41% in SPUS vs. 27% in SPY

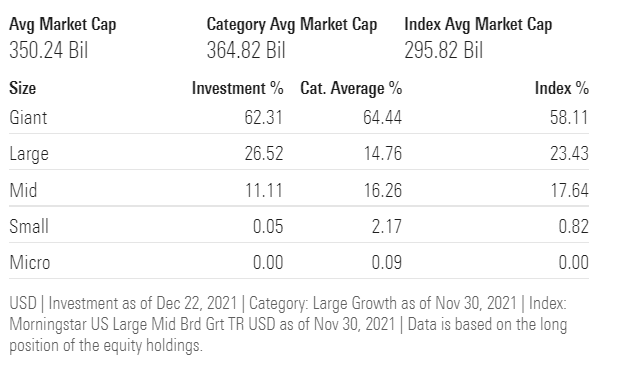

Overall, sector weights are comparable to the S&P 500 with the exception of financials/utilities due to the dependence on interest-based financing throughout those two sectors. Utilities are often highly leveraged, excluding most of them based on the debt-to-assets limit and other financial institutions profit off of interest. Most other sectors are within a few percentage points of the S&P 500 weights, except for technology which is significantly overweight. Technology is likely overweight as tech companies generally have lower leverage ratios compared to other sectors.

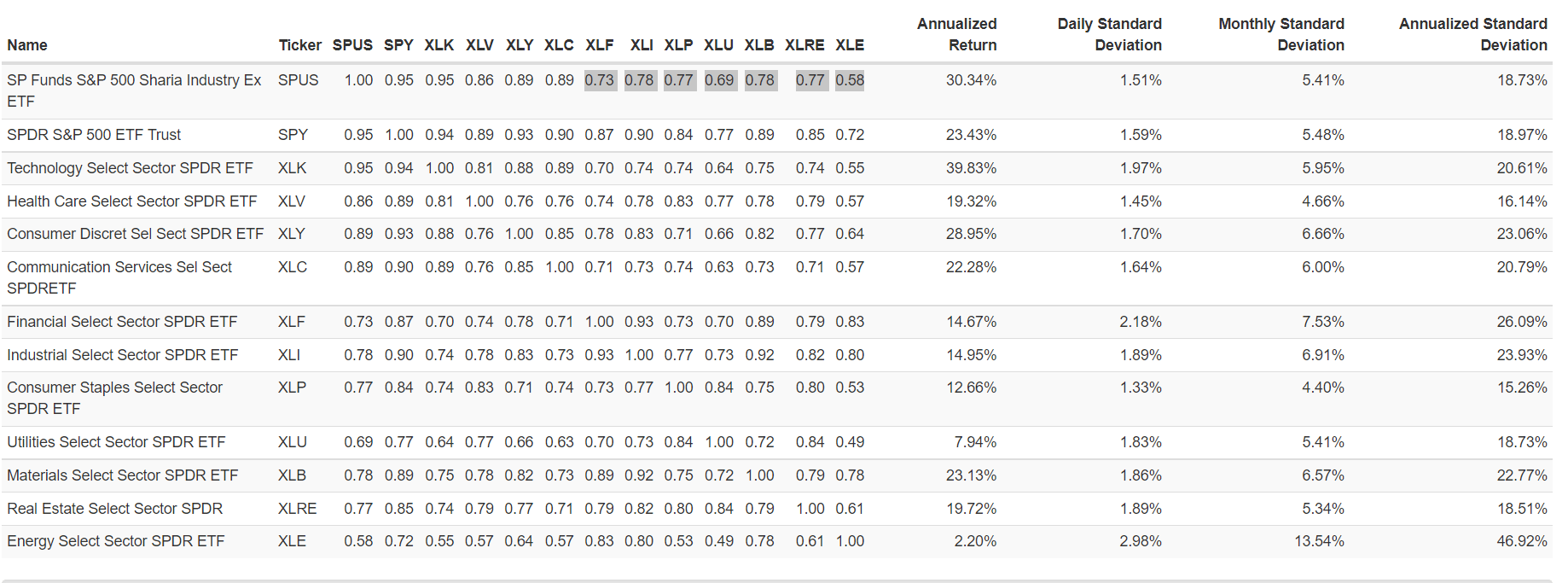

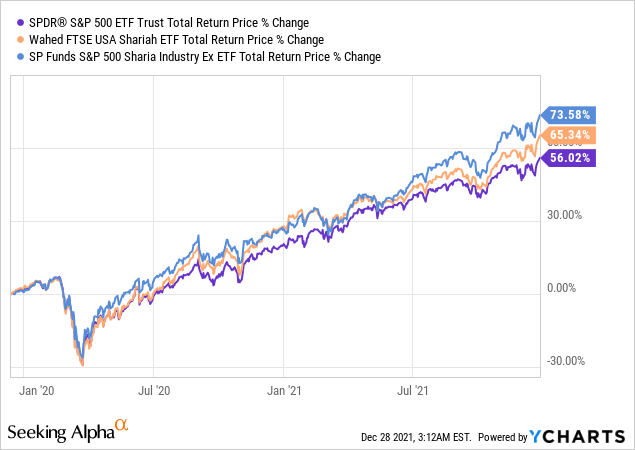

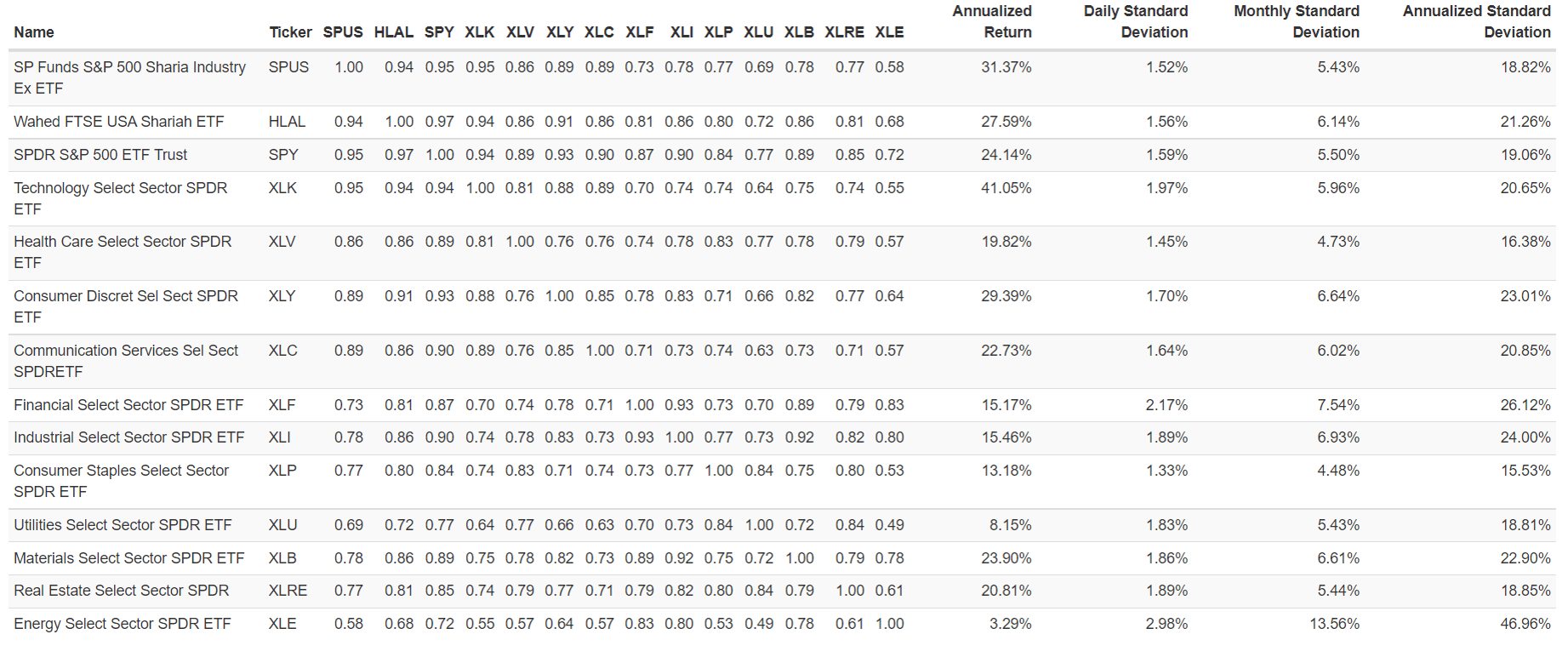

Compared to the SPDR S&P 500 ETF (SPY), this ETF has lower correlations to financials, industrials, consumer staples, utilities, real estate and energy. Overall, however, it’s highly correlated with SPY, making SPUS a good substitute for Sharia-compliant investing. It has had slightly higher returns than SPY since inception, which is mostly likely explained by the recent outperformance of tech.

Source: Generated using Portfolio Visualizer’s Asset Correlations tool

If you already have a lot of tech stocks in your portfolio, you should be mindful that this ETF is overweight tech, having about 40% of its holdings in tech, so it might not provide much diversification. You should probably calculate how much tech will be in your portfolio: add up the market value for the tech stocks you own and then add up 40% of your planned purchase amount of the ETF, divided by your total portfolio size. It would be up to you whether the total tech weighting in your portfolio will be too high; you may wish to talk to a qualified financial adviser. It might be ok if you’re bullish on tech but if you’re neutral or think tech will underperform, then you might want to limit the amount of SPUS you’d buy and look at other investment options to provide sector diversification.

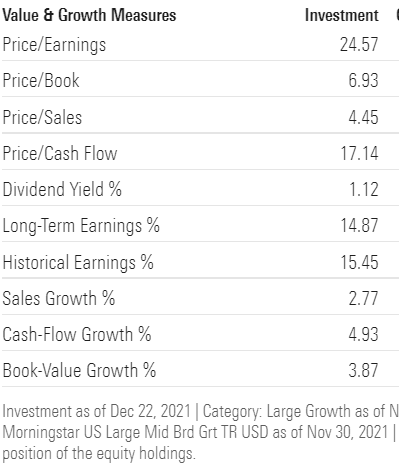

SPUS

SPUS does have significantly higher valuation ratios than SPY. This could be partially explained by SPUS having a greater percentage of mega caps than SPY, as larger cap companies tend to have higher valuation measures.

SPY

SPUS

SPY

SPUS: top 10 holdings make up 47% of its assets vs. 30% with SPY

Top exclusions:

- Amazon.com (NASDAQ:AMZN) (fails debt/equity test)

- Berkshire Hathaway Inc Class B (NYSE:BRK.B) (fails debt/equity test)

- UnitedHealth Group (NYSE:UNH) (fails debt/assets test, non-Islamic insurance)

- JPMorgan Chase (NYSE:JPM) (interest-based finance)

- Visa (NYSE:V) (interest-based finance)

- Bank of America (NYSE:BAC) (interest-based finance)

- Mastercard (NYSE:MA) (interest-based finance)

- Walt Disney (NYSE:DIS) (cinema / broadcasting)

How does it compare with the other Islamic Funds?

Wahed FTSE USA Shariah ETF (HLAL)

Expense Ratio: 0.5%

Dividend Yield: 0.9%

Holdings: 218

Index and/or Selection Universe: FTSE USA Shariah Index (based off the FTSE USA Index, that includes 600 stocks)

Top, and Top 10 Holdings %: 18.3% and 41%

HLAL invests based on the FTSE USA Shariah Index which is based on the FTSE USA Index, excluding stocks based on business activities / industries and also uses a leverage screen. The index is part of a group of FTSE Sharia compliant indices which were created by Yasaar Limited, a Sharia consulting firm made of scholars of several traditions which issues Fatwas (legal opinions/rulings by Islamic scholars) certifying investing using their indices and guidelines.

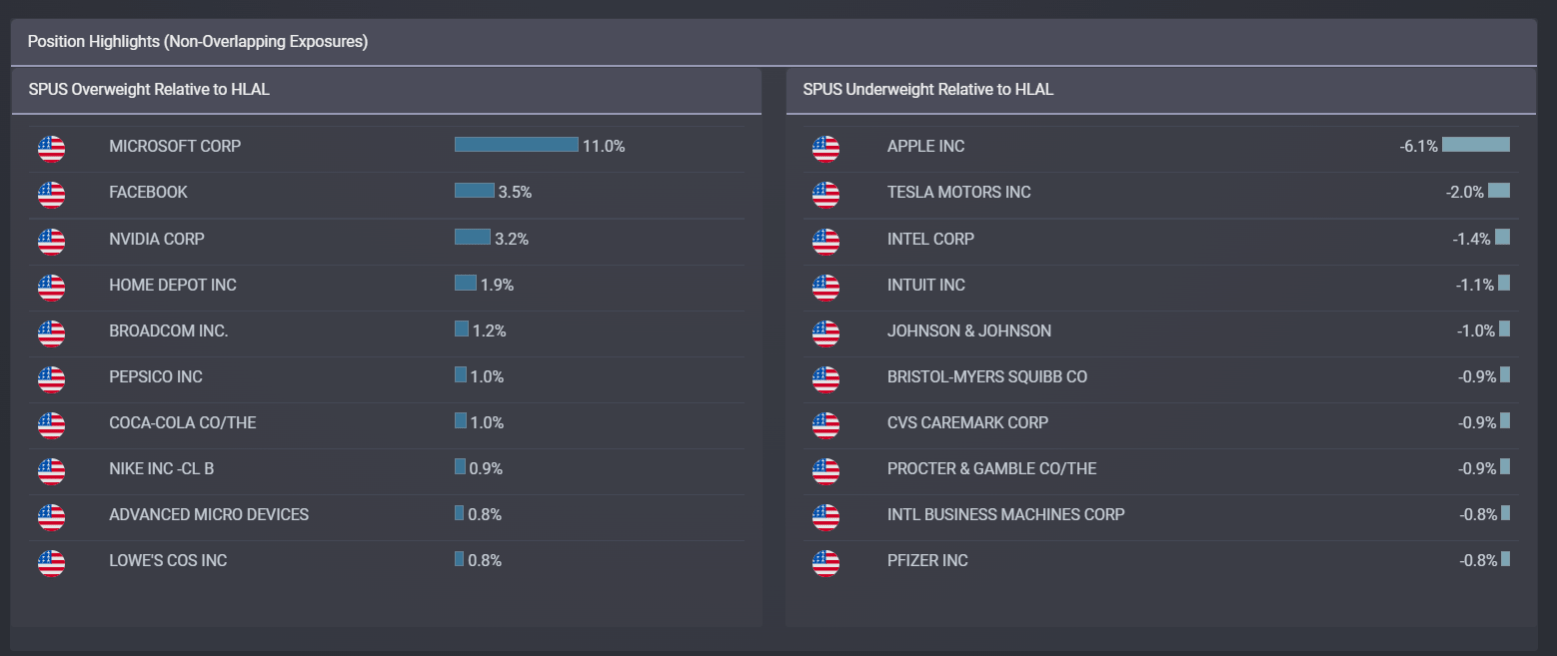

The exclusions are pretty similar to SPUS in terms of industry exclusions. Like with SPUS, it also has a leverage screen that’s pretty much identical. However, there are a few companies that are included in SPUS that aren’t included in HLAL, with Microsoft being one of them.

Source: ETF’s Fact Sheet

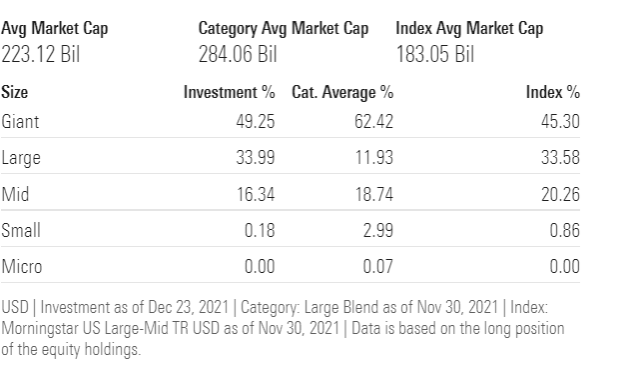

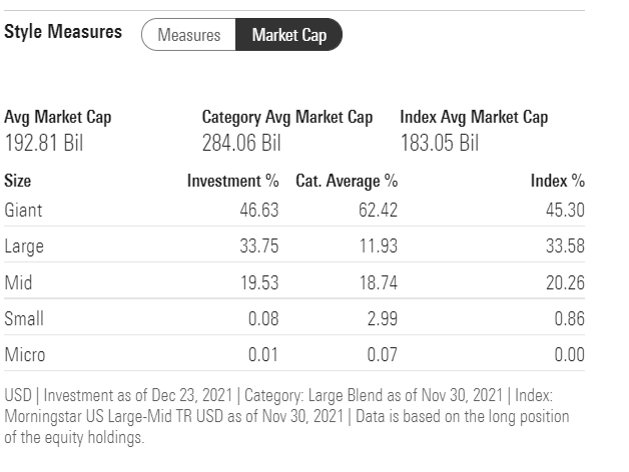

Smaller market cap on average – more mid-caps

HLAL also differs in market cap distribution, having a much smaller average market cap ($193B) than SPUS ($350B) and SPY ($223B). This is likely because HLAL is based on the FTSE USA Index which has 600 market cap weighted holdings compared to the S&P 500’s 500 holdings, so it would have some more mid-cap exposure.

Source: Morningstar

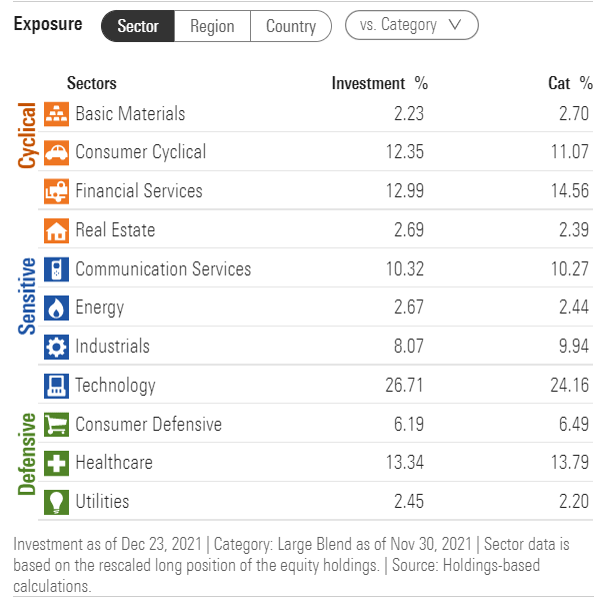

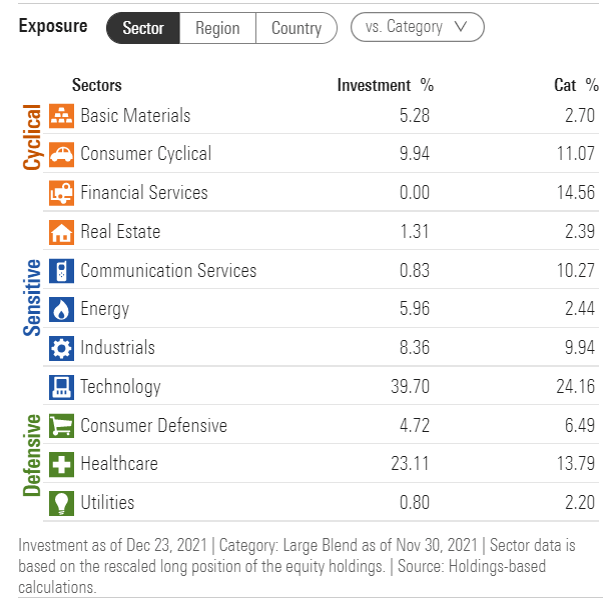

Sector Breakdown – Tech is also overweight

Source: Morningstar

This ETF has the same issue of being overweight tech, having about the same weighting as SPUS. Healthcare is also overweight in HLAL, having 23% vs. 16% in SPUS and 13% in SPY. Communication services are underweighted in HLAL, with it having 1% vs. 11% in SPUS and 10% in SPY. Energy is also overweight having 6% vs. 3% in SPUS and SPY.

HLAL has no financial sector holdings (which is the same in SPUS) due to there being no major Sharia-compliant financial institutions within the S&P 500 or FTSE USA indices.

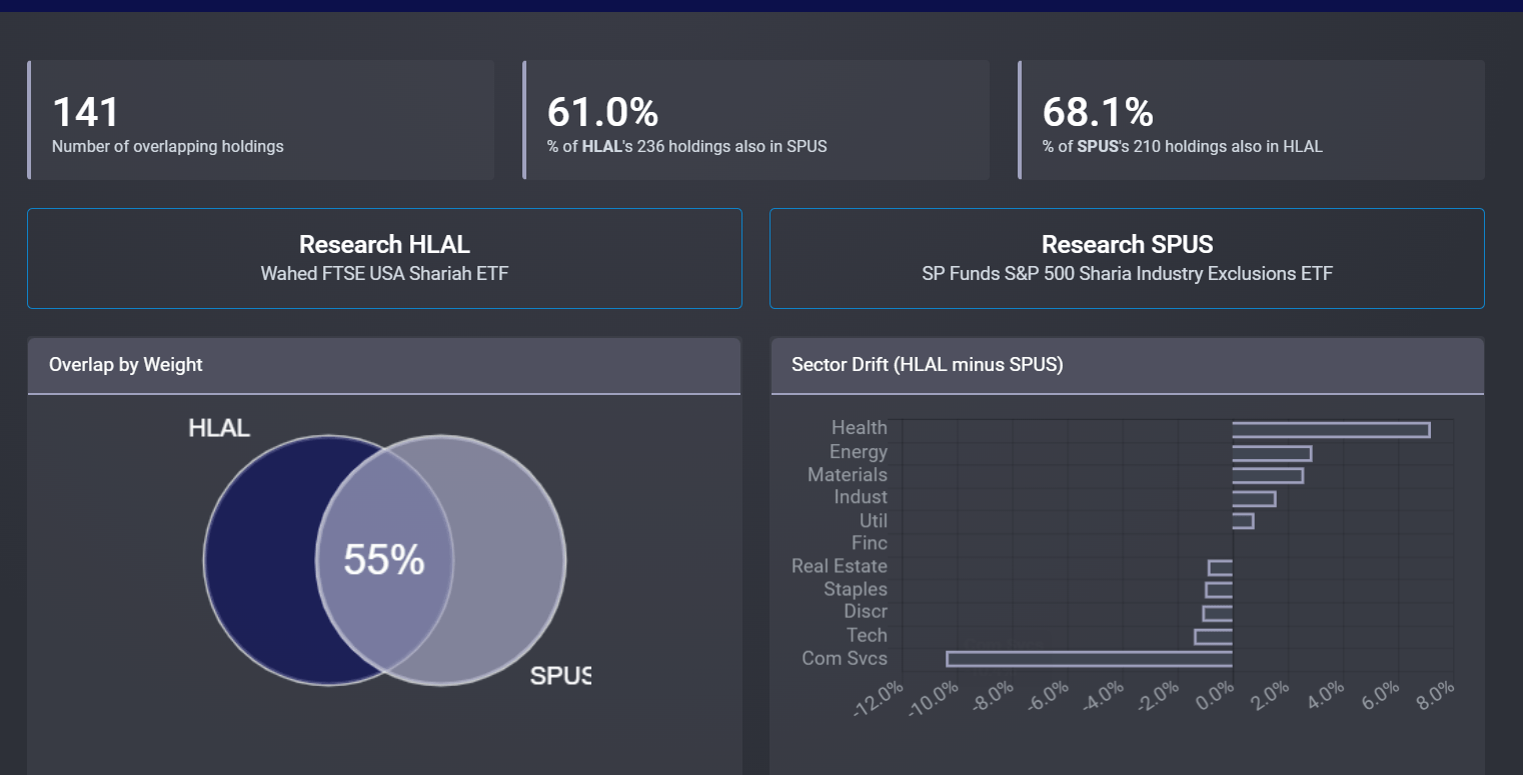

They both are about 2/3 identical with some holdings having different weightings or other holdings only being present in only one ETF. You’d still expect them to perform mostly similar as most sectors are all relatively correlated to each other and most stocks are heavily correlated to the broad stock market.

Source: ETF Research Center’s ETF overlap tool

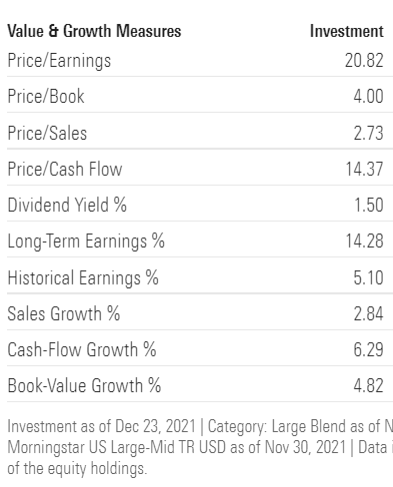

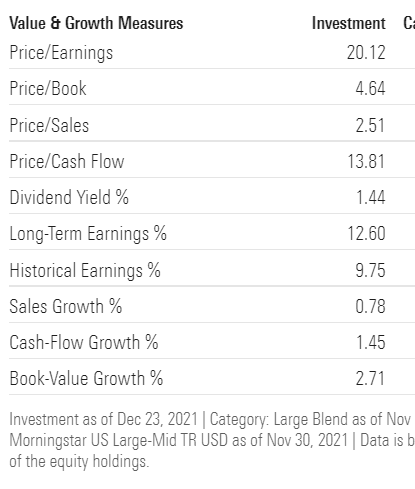

Valuations – Lower valuation measures than SPUS

While SPUS had significantly higher valuation ratios than SPY, HLAL seems to be more in line with SPY. This could be explained as it has less mega caps (which tend to have higher ratios) and more mid caps (which tend to have lower valuation ratios).

HLAL’s portfolio’s average P/E is 20.1 (24.6 for SPUS, 20.8 for SPY), P/B is 4.6 (6.9 for SPUS, 4.0 for SPY), P/S is 2.5 (4.5, 2.7), and P/CF is 13.8 (17.1, 14.4).

Source: Morningstar

Returns and Volatility

Returns are pretty comparable between the SPDR S&P 500 ETF (SPY), the Wahed FTSE USA Shariah ETF (HLAL) and the SP Funds S&P 500 Sharia Industry Exclusions ETF (SPUS). Returns for HLAL are slightly more correlated to SPY than SPUS. HLAL does have a slightly higher standard deviation at 21% (annual) vs. 19% for SPUS and SPY, likely owing to the greater ownership of mid-cap stocks; however, that’s probably not enough of a difference to be the deciding factor.

Generated using Portfolio Visualizer’s asset correlation tool.

Amana Mutual Funds

Amana is a mutual funds company offering several Sharia-compliant funds which I looked at in my previous religion investing article I wrote a few years ago. The industry exclusions are similar to the previous mentioned Sharia-compliant funds.

They have a growth fund which is overweight tech by even more than the previously mentioned ETFs. If you’re already overweight tech stocks and are looking for a way to provide some Sharia-compliant diversification to your portfolio, then you might want to consider Amana Income Mutual Fund (AMANX) instead.

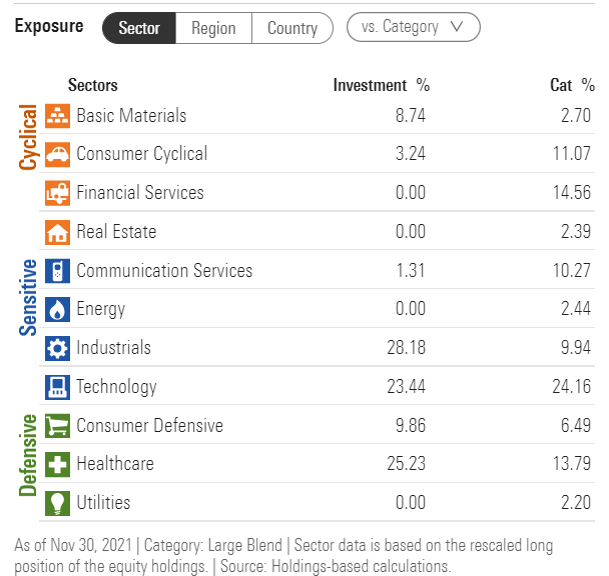

AMANX only has 34 holdings compared to 200+ in the SPUS and HLAL. Technology is only 24% of AMANX’s portfolio vs. around 40% in SPUS and HLAL. Its 3 primary sectors, making up about 3/4 of its holdings, are industrials (28%), health care (25%) and tech (24%). It is not limited to investing in the US, so may provide a bit of regional diversification.

The downsides of the Amana Income Mutual Fund are high fees (1.04%), and less flexibility in purchasing compared to ETFs (which can be traded intradaily). It has a yield of 0.85%, which is pretty poor for a dividend-stock focused fund (Vanguard’s High Dividend ETF (NYSEARCA:VYM) has a yield of 2.8%) but comparable with the yields on the other Sharia ETFs.

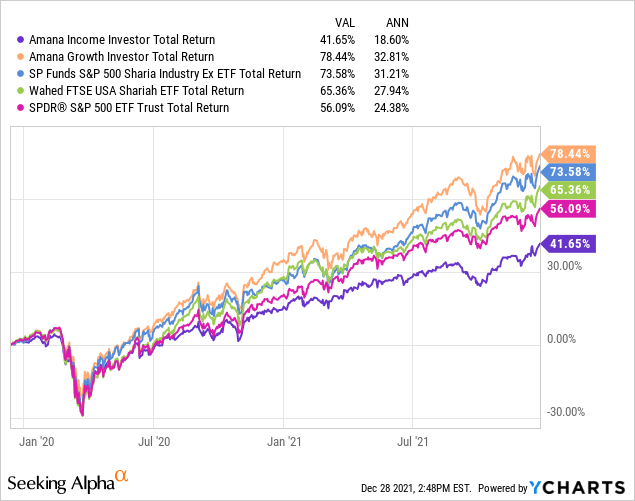

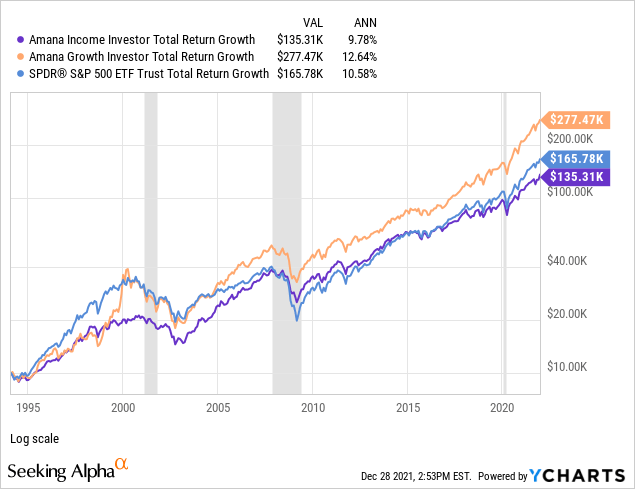

It should be somewhat less volatile and will be less prone to the ups/downs that tech has. Its long-term (over 25y) returns are about the same as SPY, but about 2.5% less annualized per year compared with the Amana Growth Mutual Fund (AMAGX).

Source: Morningstar

Final Thoughts

Investors looking to invest in a Sharia-compliant broad US fund have a few limited options: the SP Funds S&P 500 Industry-Exclusions ETF (SPUS), the Wahed FTSE Sharia USA ETF (HLAL) and Amana Mutual Funds. Both the ETFs have comparable expense ratios at 0.5% and are pretty comparable. They have some differences with the S&P 500 in terms of both being overweight tech stocks, but over the long term, they’re both pretty correlated to the S&P 500 and should have similar performance.

Which one should you pick? If you’d want more mid-cap exposure and are ok with slightly higher volatility, then HLAL is a good choice. Otherwise, if you’d want more megacaps with equivalent levels of volatility to the S&P 500, then SPUS makes sense. However, they’re both pretty comparable in terms of the criteria used to put the funds together with some minor differences. If you think that healthcare and energy sectors will outperform communication, then consider HLAL as it’s overweight healthcare and energy and underweight comms.

The Amana Growth Fund probably wouldn’t make much sense as it’s also overweight tech like the 2 ETFs but with more than double the expense ratio. The Amana Income Fund is more balanced and offers low-tech weighted broad market exposure, so at least you’d be paying extra for something more unique; it would make sense if you already have a lot of tech stocks.

If you’re looking to invest in individual stocks but don’t want to take time to check if they’re Sharia-compliant, there’s now a wide variety of app choices that can do that for you like Islamicly, Zoya, Muslim Xchange or Finispia. I have not looked into those apps, and this should not be taken as an endorsement of any of those apps as it still won’t be as accurate as manual review, so you might want to talk to a religious authority who has enough expertise in finance for advice in whether it’s suitable to use them.

Recent Comments